Marketers Most Wanted May

It’s the age of mixed media communication - and brands know it

The beginning of the new financial year has seen a surge in demand for mixed media advertising and communication, notably Social Media and Video Production. Brands use the StudioSpace platform to find talented independent agencies across a range of specialisms, and with fresh budget reallocation this month, it’s been interesting to see the high demand for expertise in these categories.

StudioSpace is an agency/client matchmaking platform, monitoring real-time briefs we receive from chief marketing officers (CMOs) and brand owners. This information gives us a unique perspective on what’s hot and what’s not each month – data which is then distilled into our monthly Marketer’s Most Wanted report.

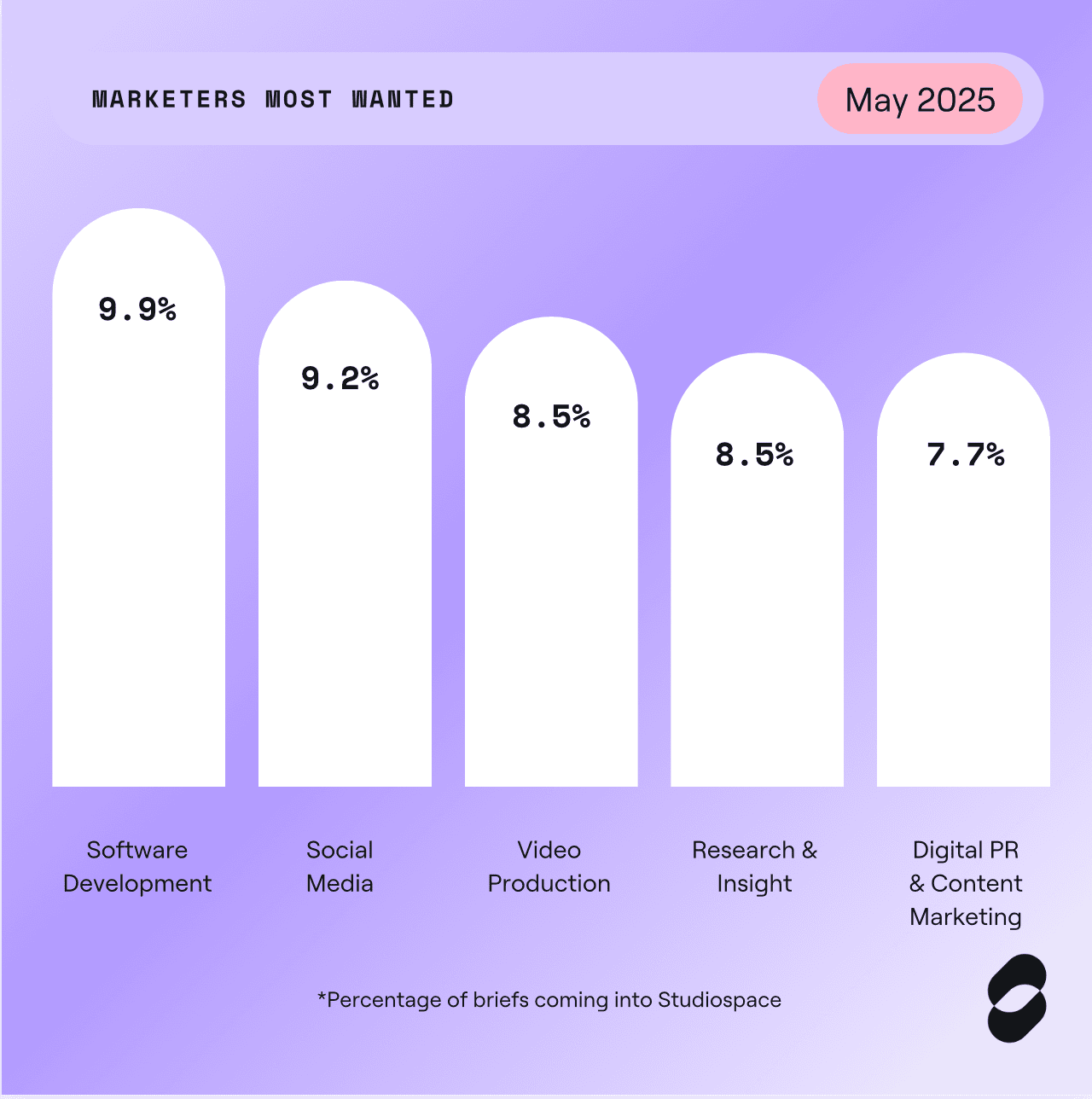

Social Media has made its return to our top three this month, after a fall to fourth place back in February. It currently sits in second, making up 9.8% of April’s total briefs. Briefs in this area include follow-on work and retained resource, as well as asks for specific campaigns. This category (then named Social Media & Content) held a first place position for almost twelve months running last year, so it’s been interesting to see volatility in 2025.

In third place is Video Production, a relatively new category which has stormed up the table this month. Its demand has risen from 7% last month (where it sat in seventh place) to 9.1% this month.

“We’re seeing demand for a real variety of video types and styles in this category,” said StudioSpace CEO Pete Sayburn. “It’s really everything from small-scale product explainers to full-scale advertising production. With attention spans seemingly limited, brands are recruiting external help to grip audiences and turn them into customers.”

Click here to browse some of our talented social and video agencies.

Software Development retains its first place position, whilst Research & Insight climbs the ladder

Software Development has retained its first place position for the second month in a row, and its top three position for the seventh. Popularity in this category has been driven by several new projects as well as extensions to existing ones - all of which vary widely in terms of scale and size. Brands are increasingly looking to add mobile apps to their digital presences, or to create standout websites that set them apart from the rest.

Having climbed from sixth place to fourth this month is Research & Insight. This category was relatively new to the table this time last year, and has held a number of different positions since its initial entry. In April, it made up 8.4% of our total briefs, compared to 7% in March. As Gen Alpha joins the consumer market, brands are looking for external support to research their new audience(s). Competitor intelligence is another key feature of this category, and in an ever-evolving market, this feature looks to be high demand for the foreseeable.

“It’s encouraging to see that brands are reinvesting in research and insight, as it looks like fresh financial year budgets are enabling teams to explore new markets,” said Sayburn. “We expect that this may drive investment in other areas, especially Product & Proposition and Experience Strategy & Design.”

Digital PR & Content Marketing, Integrated Digital Marketing and UX/UI Design all experience a fall this month

Digital PR & Content Marketing has dropped down the table after its entry at second as a new category last month. It currently represents 8.4% of briefs, a fall from 9.2% in March. This category includes digital PR, and all aspects of digital content creation - from copywriting, editorial, graphic design, and video editing. Given the smaller average project size we expect the volume of projects to fluctuate month on month. The positioning of this category certainly adds to our earlier point about brands recognising the importance of strong digital communication, and investing as such.

Our Integrated Digital Marketing category also experienced a fall this month, from third place last month (8.5%) to sixth this month (7.7%). This category has been a consistent member of the table since March 2024, but its position has changed each month, occupying almost every position over the last year. It will be interesting to see whether demand in this area picks up this summer.

Despite retained solid demand in this category, UX/UI Design is down two places from last month - fifth to seventh. We’re not yet seeing signs of a surge up the table, but with clear investment in digital transformation elsewhere, this may change!

Product & Proposition retains its position

Product & Proposition, another of our reimagined categories, has retained both its position and proportion this month. It sits comfortably in eighth place, making up 6.3% of total briefs. Proposition Design - as it was formally called - was a real table mover last year, depending on budget availability for innovation, so we can certainly expect this category to pick up again now that the new financial year has properly begun.

Digital Paid Media is our latest entry

Digital Paid Media is a new entry at number nine this month, representing 5.6% of our total. This category covers all aspects of performance marketing including paid social, PPC, paid search engine marketing and demand generation.

“Its entry alongside the popularity of Social Media, Digital PR and Digital Marketing shows that digital marketing overall is high in demand - these categories together make up 31.5% of total briefs this month, showing that digital is where brands are placing a lot of investment in the StudioSpace platform,” said Pete.

Ones to watch this summer

Experience Strategy & Design has dropped a spot this month, now sitting in tenth place. In this category, we’re seeing demand to both reimagine existing experiences and develop new ones, with a focus on omnichannel delivery and a splash of service design.

This category usually rises in demand over the summer period, where brands reshuffle their looks and focus on events.

Other categories to watch out for this summer - which didn’t quite make the table this month - include Creative Campaign and Brand Strategy. We labelled summer 2024 the ‘Summer of Creativity’, so it will be interesting to see whether these upcoming months are similar.

Conclusion

In conclusion, the digital landscape is evolving rapidly, with brands making significant investments in digital capabilities. The surge in demand for Social Media and Video Production reflects a clear shift towards enhancing online presence and engagement. Additionally, the rise of Research & Insight highlights the growing focus on understanding new audiences, particularly with Gen Alpha emerging as a key demographic. As we move through 2025, these shifts underscore the increasing importance of digital expertise, and the need for brands to adapt quickly to stay competitive in a fast-changing market.